Insights

Search through our most active topics and see how they are helping clients discover new potential and implement positive change.

IFRS

TAX

LAWS

International Financial Reporting Standards (IFRS)

Replaces IAS 1. Changes how you present financial performance, not how you measure it. All income and expenses must now be classified into defined categories.

Income & expense categories

+ Operating - Core business income and expenses

The default category — anything not classified elsewhere goes here. It reflects your main business activities.

- Revenue from sales of goods or services

- Cost of goods sold and operating expenses

- Salaries, rent, utilities

- Impairment losses on operating assets

Produces the new mandatory subtotal: Operating profit or loss.

+ Investing - Returns from assets outside core operations

Income and expenses from assets that generate returns independently of main operations.

- Dividends received from equity investments

- Interest earned on loans to third parties

- Gains or losses on disposal of investments

- Share of profit from associates & joint ventures

Assets used daily in operations (e.g. machinery) stay in Operating, not here.

+ Financing - Cost of raising & Servicing capital

Covers costs from liabilities used to raise finance — the cost of borrowing money.

- Interest expense on bank loans and bonds

- Interest on lease liabilities (IFRS 16)

- Gains or losses on early repayment of debt

- Transaction costs on issuing or repaying loans

Trade payables and operating-related liabilities stay in Operating.

+ Discontinued operations - Business being wound down or sold

Results from a business segment disposed of or held for sale — keeps ongoing performance separate from one-off exits.

- All income & expenses of the discontinued segment

- Gain or loss on disposal of the segment

- Re-measurement to fair value less costs to sell

Shown as a single line on the income statement; detail disclosed in the notes.

Important Note - Comparative 2026 figures must be restated - businesses should begin preparation now.

Governs when and how much revenue to recognise. Replaces IAS 11 & IAS 18 with a single, consistent 5-step model that applies to virtually every business selling goods or services.

The 5-step revenue recognition model:

- Step 1 — Identify the contract

Written, oral or implied agreements that create enforceable rights and obligations between both parties.

- Step 2 — Identify performance obligations

Break the contract into distinct promises. A product bundled with a warranty may be two separate obligations.

- Step 3 — Determine the transaction price

Total amount expected to be received, including estimates for variable elements like bonuses or discounts.

- Step 4 — Allocate price to each obligation

Split the price between obligations based on their standalone selling prices.

- Step 5 — Recognise revenue when obligation is satisfied

At a point in time (goods delivery) or over time (services, construction contracts).

Requires almost all leases to appear on the balance sheet as an asset and a liability, bringing hidden obligations into the open.

What changes on your financial position

> Right-of-use asset

When you sign a lease, you record an asset representing your right to use that item - office, vehicle, equipment. It is depreciated over the lease term.

> Lease liability

The present value of all future lease payments, recorded as a financial obligation. Interest expense is recognised separately each period.

Practical exemptions

Short-term leases — 12 months or less

Low-value assets — e.g. laptops, small office equipment

Putting leases on financial position increases reported debt, which can affect loan covenants and credit ratings. Review your leasing agreements now.

Bahrain TAX & Value Added Tax (VAT)

The 2025–2026 budget approved in March 2025 outlined plans to implement a broad corporate tax, and the upcoming Bahrain CIT is expected to include specific provisions related to capital gains tax and transitional rules.

On 29 December 2025, the Bahraini Cabinet approved the introduction of Corporate Income Tax (“CIT”) in Bahrain, with implementation anticipated from 2027. Based on the Cabinet’s announcement, Bahrain is expected to introduce a 10% CIT applicable to businesses that meet either of the following thresholds:

- Annual revenues exceeding BHD 1 million, or

- Net annual profits exceeding BHD 200,000.

What is CIT?

Corporate Income Tax (CIT) is a direct tax levied on taxable income earned by a taxable person during a financial year. CIT is generally assessed through an annual tax return and may be subject to audit by the tax authority. In Bahrain, taxable persons could include companies, establishments, branches of foreign entities, and individuals whether or not commercially registered-who are considered to be carrying on a business.

Capital gains on the disposal of assets are expected to be taxable, with potential exemptions subject to meeting conditions (for example, group restructuring). Transitional provisions should prevent taxation of gains generated prior to CIT go-live.

Alert >> With CIT on the horizon, businesses should act in three phases: first, assess the impact on your current structure, operations, and related-party transactions; then, once regulations are released, address transitional rules, tax accounting adjustments, and ERP readiness; and finally, get your administration in order, covering tax registration, filing processes, transfer pricing documentation, and audit preparedness.

Bahrain Regulatory General Topics

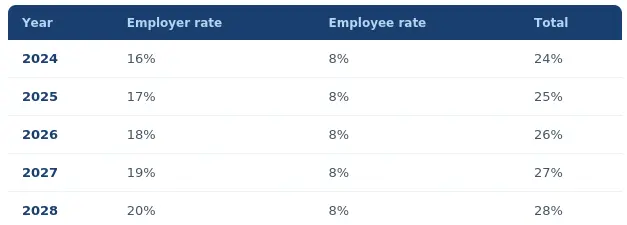

Law No. (14) of 2022 amended Bahrain's Social Insurance Law (Decree-Law No. 24 of 1976), introducing mandatory annual 1% increases to employer contributions from 2023 to 2028, aiming to improve long-term sustainability. Key reforms include increasing employer contributions to 17% in 2025 and 18% in 2026 for Bahraini workers, while employee contributions remained unchanged at 8% (inclusive of 1% unemployment insurance).

Contribution schedule:

Bahrain Edict No. 109 of 2023, issued by the Prime Minister in December 2023, establishes a new end-of-service gratuity system for non-Bahraini workers in the private sector. It requires employers to remit gratuity contributions to the Social Insurance Organisation (SIO) monthly rather than paying them directly upon termination, effective March 1, 2024.

Monthly contribution rates

:

- First three years of service 4.2% of monthly wage (~½ month's wage per year).

- Each year beyond 3 years 8.4% of monthly wage (~1 month's wage per year).

Note - EOSB accrued before 1 March 2024 remains the employer's direct responsibility, to be paid upon termination in the traditional way.